How To Calculate Balancing Charge And Balancing Allowance Malaysia : Calculate The Capital Allowance Residual Expenditure And Balancing Charges Course Hero / In this case as a company u would get a benefit of £2000 i.e.

How To Calculate Balancing Charge And Balancing Allowance Malaysia : Calculate The Capital Allowance Residual Expenditure And Balancing Charges Course Hero / In this case as a company u would get a benefit of £2000 i.e.. To calculate the balancing charge, add the amount you sold the item for to the capital allowances you claimed, then subtract the amount you originally bought the item for. However, the amount of the balancing charge should not exceed the total capital allowances allowed. 7.1 balancing allowance balancing allowance arises when the disposal value of a plant or machinery is less than the residual expenditure. Example of a balancing charge: While annual allowance is a flat rate given every year based on the original cost of the asset.

Balancing allowance & charges calculation. 3.7 balancing charge is the excess that arises where the sale price of a plant, machinery or industrial building which is purchased/constructed and used in/for the purposes of the business exceeds the residual expenditure of that asset. In a controlled transfer, no balancing charge or balancing allowance will arise to the seller and the acquirer can continue to claim capital allowances on the transferred asset, subject to the tax residual value of the asset. 4 years later, you sell the laptop on ebay for £500. Enter the date of acquisition or any date in a prior accounting period.

7 Steps To Calculating Estimated Chargeable Income Eci Tinkertax from tinkertax.com If machine b is scrapped (no proceeds) you get an additional balancing allowance, which is treated as a normal capital allowance. Demonstration of balancing charge in binary ionic compounds 3.7 balancing charge is the excess that arises where the sale price of a plant, machinery or industrial building which is purchased/constructed and used in/for the purposes of the business exceeds the residual expenditure of that asset. In this case as a company u would get a benefit of £2000 i.e. To calculate the balancing charge, add the amount you sold the item for to the capital allowances you claimed, then subtract the amount you originally bought the item for. The qualifying expenditure (qe) incurred by the acquirer and the date the asset is deemed to have been acquired by the acquirer is determined in accordance with the itr 1969. Computation of capital allowances and balancing charge. Capital gain is an economic concept defined as the profit.

Capital gain is an economic concept defined as the profit.

If the asset is disposed of then there will always be a balancing charge or allowance and therefore a tax effect (a balancing allowance gives rise to a tax saving, a balancing charge gives rise to more tax payable). However, the amount of the balancing charge should not exceed the total capital allowances allowed. To calculate the balancing charge, add the amount you sold the item for to the capital allowances you claimed, then subtract the amount you originally bought the item for. While annual allowance is a flat rate given every year based on the original cost of the asset. Example of a balancing charge: As this is more than the tax written down value, you must add a balancing charge to your annual profit when you do your tax return. Annual allowance rates vary according to the type of the assets and the rates tabulated in the table below. When a fixed asset is sold or written off, you need to calculate balancing allowance (ba) or balancing charge (bc) if capital allowance has been claimed for the asset previously. 1) sold the machine for £18,000. In this case as a company u would get a benefit of £2000 i.e. Balancing adjustments (allowance / charge) will arise on the disposal of assets on which capital allowances have been claimed. The purchase price are ignored and no balancing allowance or balancing charge is imposed on the disposer. Im preparing my own tax rtn here (mine always left till last minute!) and i am dealing with capital allowances on cars.

Since this is a addition benefit, it would be taxable referred as balancing charge. The balancing charge is calculated as follows: To enter a balancing charge/allowance for an asset that you've written off in a previous year, follow these steps: Laptop sale price (£500) + capital allowances claimed (£2,000) minus the original laptop price (£2,000) = £500. These can arise in certain circumstances (for example, when your business ceases, or you sell an asset for more than the total written down value of the pool).

Chapter 7 Capital Allowances Students from image.slidesharecdn.com This balancing charge is subject to tax. When a fixed asset is sold or written off, you need to calculate balancing allowance or balancing charge if capital allowance has been claimed for the asset previously. The balancing allowance is allowed as a deduction from. Im preparing my own tax rtn here (mine always left till last minute!) and i am dealing with capital allowances on cars. In this case as a company u would get a benefit of £2000 i.e. The balancing charge is restricted to the total capital allowances claimed by the disposer. The balancing charge is calculated as follows: 4.4 balancing allowance refers to the difference where the disposal value of an asset is less than the residual expenditure.

The balancing allowance is allowed as a deduction from.

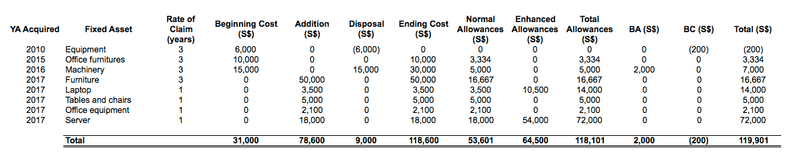

Balancing charge 2,080 2,080 moveable machinery assets ceased to be used on 2 may 2018, no capital allowance claimed nil the assets were classified as assets held for sale in ya 2018 but the sale will not be completed until after 31 may 2018, so the balancing adjustment calculation will only be made in ya 2019 nil customer database nil Gains arising from the sale of shares in a real property company or real property (for example, land and buildings) Home > businesses > companies > working out corporate income taxes > claiming allowances > capital allowances > selling or scrapping fixed assets when a fixed asset is sold or written off, you need to calculate balancing allowance (ba) or balancing charge (bc) if capital allowance has been claimed for the asset previously. Balancing adjustments (allowance / charge) will arise on the disposal of assets on which capital allowances have been claimed. A balancing charge is the opposite of a capital allowance, which reduces the amount of profit you have to pay tax on. Balancing allowance is tax deductible whereas balancing charge is taxable income. Balancing charge and balancing allowance. The tax written down value is the amount you bought the item for, minus any capital allowances you claimed. Choose the type of asset (whichever pool the asset was initially entered in). To enter a balancing charge/allowance for an asset that you've written off in a previous year, follow these steps: Laptop sale price (£500) + capital allowances claimed (£2,000) minus the original laptop price (£2,000) = £500. When a fixed asset is sold or written off, you need to calculate balancing allowance or balancing charge if capital allowance has been claimed for the asset previously. A tax treatment in relation to qualifying expenditure on plant and machinery for the purpose of claiming capital allowances.

Balancing allowance or balancing charge arises only when an initial allowance (ia) and annual allowances (aa) have been given or may be given if claimed. Example of a balancing charge: The purchase price are ignored and no balancing allowance or balancing charge is imposed on the disposer. Atxb213 malaysian taxation 1 10 11. In a controlled transfer, no balancing charge or balancing allowance will arise to the seller and the acquirer can continue to claim capital allowances on the transferred asset, subject to the tax residual value of the asset.

How To Calculate Balancing Charge And Balancing Allowance Malaysia Afiit from 2.bp.blogspot.com Computation of capital allowances and balancing charge. A balancing allowance is a type of capital allowance which can be given under several of the allowance codes when an asset is disposed of or the business comes to an end. This balancing charge is subject to tax. The qualifying expenditure (qe) incurred by the acquirer and the date the asset is deemed to have been acquired by the acquirer is determined in accordance with the itr 1969. The balancing allowance is allowed as a deduction from. When a fixed asset is sold or written off, you need to calculate balancing allowance (ba) or balancing charge (bc) if capital allowance has been claimed for the asset previously. If the asset is disposed of then there will always be a balancing charge or allowance and therefore a tax effect (a balancing allowance gives rise to a tax saving, a balancing charge gives rise to more tax payable). When a fixed asset is sold or written off, you need to calculate balancing allowance or balancing charge if capital allowance has been claimed for the asset previously.

In this case as a company u would get a benefit of £2000 i.e.

A balancing charge or allowance (that is, an adjustment to the quantum of the allowances made) may arise in a chargeable period where any of the following events occurs in relation to any machinery or plant in respect of which capital allowances have been obtained by a person carrying on a trade — I sold my car to my parents last dec and made a loss of a few grand, i know this is a balancing allowance, is the allowance the 'actual' loss amount i.e 2000 or is it 2000 x 25%? In this case as a company u would get a benefit of £2000 i.e. For more information about these allowances see page 4 of this helpsheet. The balancing allowance is allowed as a deduction from. 4.6 plant for the purpose of qualifiying expenditure means any movable or Home > businesses > companies > working out corporate income taxes > claiming allowances > capital allowances > selling or scrapping fixed assets when a fixed asset is sold or written off, you need to calculate balancing allowance (ba) or balancing charge (bc) if capital allowance has been claimed for the asset previously. The balancing charge is calculated as follows: The purchase price are ignored and no balancing allowance or balancing charge is imposed on the disposer. The balancing charge is restricted to the total capital allowances claimed by the disposer. To enter a balancing charge/allowance for an asset that you've written off in a previous year, follow these steps: Example of a balancing charge: However, the amount of the balancing charge should not exceed the total capital allowances allowed.

Related : How To Calculate Balancing Charge And Balancing Allowance Malaysia : Calculate The Capital Allowance Residual Expenditure And Balancing Charges Course Hero / In this case as a company u would get a benefit of £2000 i.e..